|

|

||||||

|

|

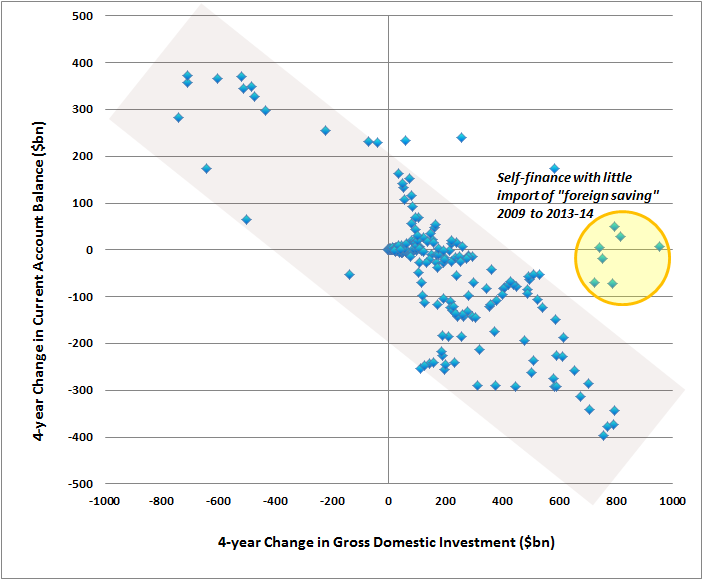

April 20, 2015 Profit Margins - Is the Ladder Starting to Snap? Since mid-2014, the broad market as measured by the NYSE Composite has been in a broad sideways distribution pattern, with an increasing tendency in recent months for advances to occur on weaker volume and declines to follow on a pickup in volume. While capitalization-weighted indices have done somewhat better since mid-2014, the S&P 500 Index is unchanged since late-December. On the basis of broad market action across individual stocks, industries, sectors and security types, as well as a general widening of credit spreads and other risk-sensitive measures, we continue to infer a shift toward increasing risk-aversion among investors. On the valuation front, we should begin by emphasizing that the most historically reliable valuation measures – those most closely related to actual subsequent market returns over full-cycle horizons of about 7 years or more – are those that adjust for the cyclical variation of profit margins (see Margins, Multiples and the Iron Law of Valuation). Indeed, on a 10-year horizon, these measures are generally about 90% correlated with actual subsequent total returns in the S&P 500, and this relationship has persisted even in recent market cycles. Though it’s not widely recognized, measures such as the ratio of market capitalization/nominal GDP and the S&P 500 price/revenue ratio are actually better correlated with actual subsequent total market returns than price/operating earnings ratios, the Fed model, and even the raw Shiller P/E (though the Shiller P/E does quite well once one adjusts for the embedded profit margin). To fully understand the present valuation extreme, recognize that the market cap/GDP ratio is currently about 1.29 versus a pre-bubble norm of just 0.55, with “secular” lows such as 1982 taking the ratio to about 0.33. To fully understand the present valuation extreme, recognize that the S&P 500 price/revenue ratio is currently about 1.80, versus a pre-bubble norm of just 0.8, with “secular” lows taking the ratio to about 0.45. To put these figures in perspective, if we assume that nominal GDP and corporate revenues will grow perpetually at a 6% nominal rate (which is much faster than we actually observe here), and the market does not experience another secular market low until 2040 – a quarter century from now, the S&P 500 Index would still be approximately unchanged from current levels at that secular low 25 years from today. The arithmetic here is relatively simple. For market cap/GDP the annual percentage change of the S&P 500 Index over that 25 year period would be (1.06)*(0.33/1.29)^(1/25)-1 = 0.37%. For the price/revenue ratio, the calculation would be (1.06)*(0.45/1.8)^(1/25)-1 = 0.28%. In both cases, dividend income would result in a somewhat higher total return over that quarter-century horizon. One obtains less extreme conclusions, though still uncomfortable, if one assumes that these multiples simply touch their pre-bubble norms a decade from now. In that case, the annual percentage change in the S&P 500 Index over the coming decade would be -2.67% and -2.26%, respectively. If all of this seems preposterous, keep in mind that these revolting long-term prospective returns in stocks are simply a less recognized variant of what we observe more clearly in the bond market, where long-term interest rates are now negative in about one third of the developed world. Investors are literally paying their governments for the privilege of lending to them on a 5-10 year horizon. Investors are collectively out of their minds if they believe that current equity prices don’t quietly reflect the same absurd state of affairs. We’re not talking about dusty, arcane valuation levels that investors can assume will never be seen again. Indeed, market valuations fell below pre-bubble norms even during the most recent market cycle (see Why Warren Buffet is Right and Why Nobody Cares). Deviations in valuation from historical norms have reliably been associated with similar deviations in long-term returns from their historical norms - which is why the S&P 500 has posted a total return of less than 4% annually over the past 15 years - and even then only because valuations have again been pushed to bubble extremes. Understand also that these valuation measures haven’t missed a beat in a century of market cycles. Our objective isn't to convince anyone to abandon their own disciplines - only to clearly lay out the current situation for those who value our work. I've been very open about the awkward transition that resulted from my 2009 insistence on stress-testing our methods against Depression-era data (see A Better Lesson than “This Time is Different” for a discussion of how we addressed those challenges). But recognize that our valuation methods haven’t changed. The same methods accurately identified extreme overvaluation in 2000, improved enough to encourage a constructive shift in early 2003 as a new bull market was emerging, accurately identified extreme overvaluation in 2007, improved enough to recognize undervaluation in 2008-2009, and now identify the third valuation bubble in 15 years – one that we expect will conclude no better than the first two. As I frequently emphasize, a resumption of favorable market internals and a retreat in credit spreads would suggest a fresh shift toward risk-seeking investor preferences that could defer the immediacy of our downside concerns. Unfortunately, that would not improve the dismal long-term returns that are already baked in the cake of current valuations. Presently, we observe obscene valuations coupled with evidence of a shift toward increasing risk-aversion among investors. For that reason, I continue to believe that the present moment will likely be remembered among a small handful of the very worst points in history to invest in equities from the standpoint of prospective return and risk. Profit margins – is the ladder starting to snap? One of the central features of popular valuation measures such as price to forward earnings is that they take profit margins at face value. Year-ahead earnings estimates have the additional feature that analysts can (and nearly always do) base their estimates on the assumption that margins will improve in the future. We know from a century of evidence that correcting for the variation in profit margins produces valuation measures that are far better correlated with actual subsequent market returns. But when profit margins are elevated, the temptation to take them at face value (or extrapolate them to even greater extremes) seems too much for Wall Street to resist. Though it’s typically not appreciated by investors, the deficits of one sector of the economy are (and must be) offset by surpluses in other sectors. As detailed in An Open Letter to the FOMC: Recognizing the Valuation Bubble in Equities, this relationship is captured by what economists know as the “savings-investment identity,” which can also be expressed as the Kalecki profits equation: Corporate Profits = (Investment – Foreign Savings) – Household Savings – Government Savings + Dividends In this equation, investment means gross domestic investment – real things like capital equipment and housing. Foreign savings are essentially the inverse of the U.S. current account balance. The reason I place parentheses around (Investment – Foreign Savings) is that in U.S. data, increases in gross domestic investment are typically accompanied by deterioration in the current account balance, while an increasing current account balance is typically accompanied by falling gross domestic investment. Because variations in those two components largely cancel out, and because dividends aren’t terribly variable, it turns out in U.S. data that the majority of variation in corporate profits over time is a mirror image of variation in the sum of household and government savings. Elevated corporate profits since 2009 have largely reflected mirror image deficits in the household and government sectors, as households have taken on debt to maintain consumption despite historically low wages as a share of GDP, and government transfer payments have expanded to fill the gap, with 46 million Americans now on food stamps – a five-fold increase in expenditures since 2000. Essentially, corporations are selling the same volume of output, but paying a smaller share in wages, with deficits in the household and government sectors bridging the gap. As households and government have shoveled themselves further into the hole, corporate profits have climbed higher on the adjacent pile of earth. Deficits of one sector emerge as the surplus of another. While that story explains most of the rise in corporate profits, they’ve also climbed an additional ladder. As noted earlier, changes in gross domestic investment are usually reflected by mirror-image movements in the current account balance. But since 2009, we’ve seen a recovery in real investment from the worst lows of the financial crisis, but without the usual deterioration in the current account. The chart below shows this as the scatter of data points in yellow. In recent months, there is evidence that this outlier is beginning to reverse, as investment activity is slowing even as the current account balance is going south.

This puts us on renewed alert for deterioration in profit margins. From the Kalecki equation we can ask the following question. What happens to corporate profits in an environment of softening real investment activity (with new orders plunging for durables and other output)? Since variations in dividends have minimal impact in the Kalecki equation, the answer is that the outcome for profits depends primarily on three things: foreign savings (the inverse of the trade balance), private savings, and government savings. If those forms of savings are all increasing, and real investment is relatively flat, corporate profits must retreat. So let’s take a look. On the current account, the strong U.S. dollar is beginning to take its toll on the trade balance, pushing the U.S. deeper into deficit in recent months. For purposes of the Kalecki equation, that means a rising “foreign savings” component, which enters the equation with a negative sign. That is, other things being equal, a worsening current account deficit is a negative for U.S. corporate profits.

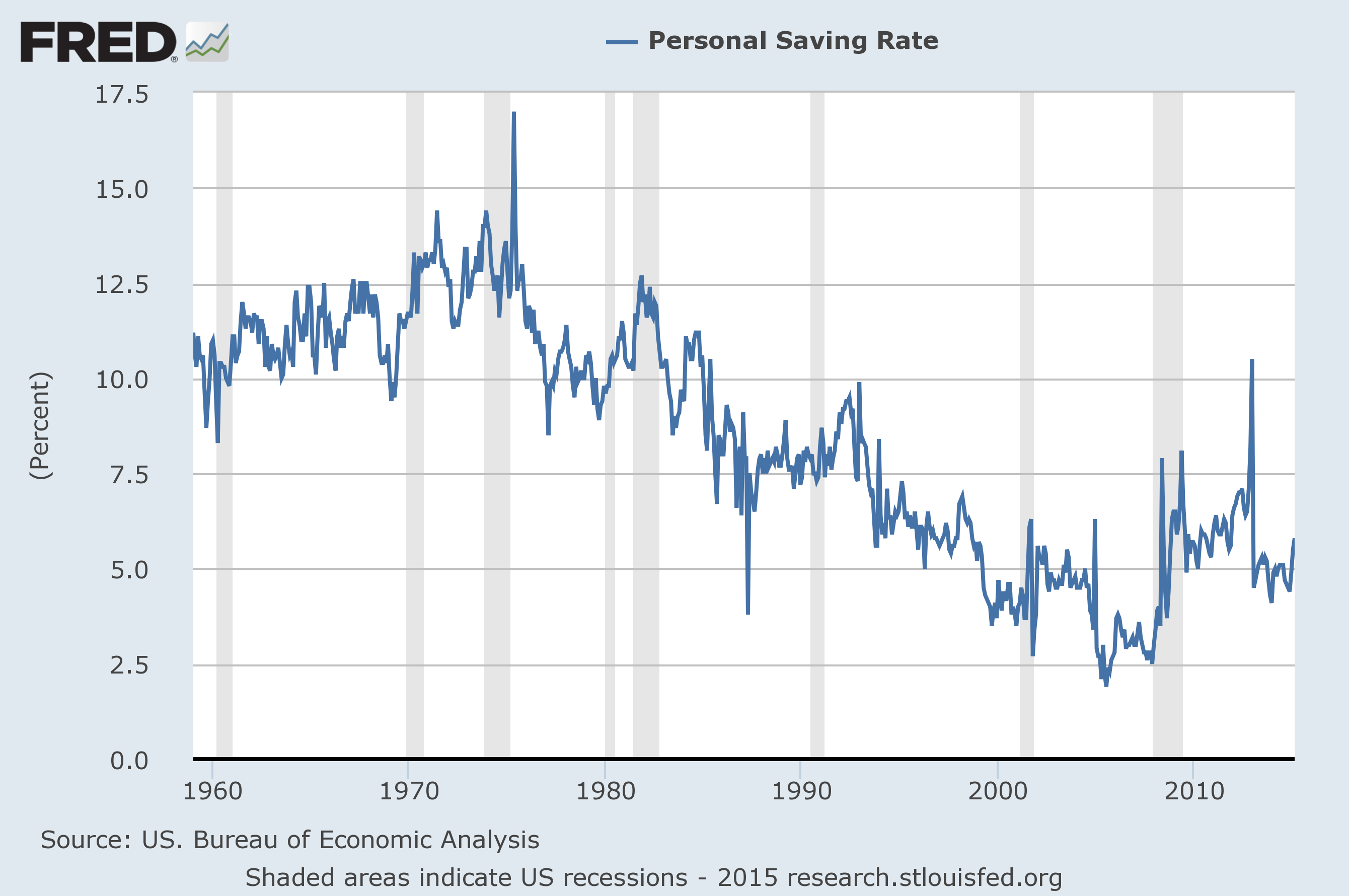

What about household savings? Increasing. Look again at the Kalecki equation. Increasing household savings (particularly in an environment of slowing real investment) are a negative for U.S. corporate profits.

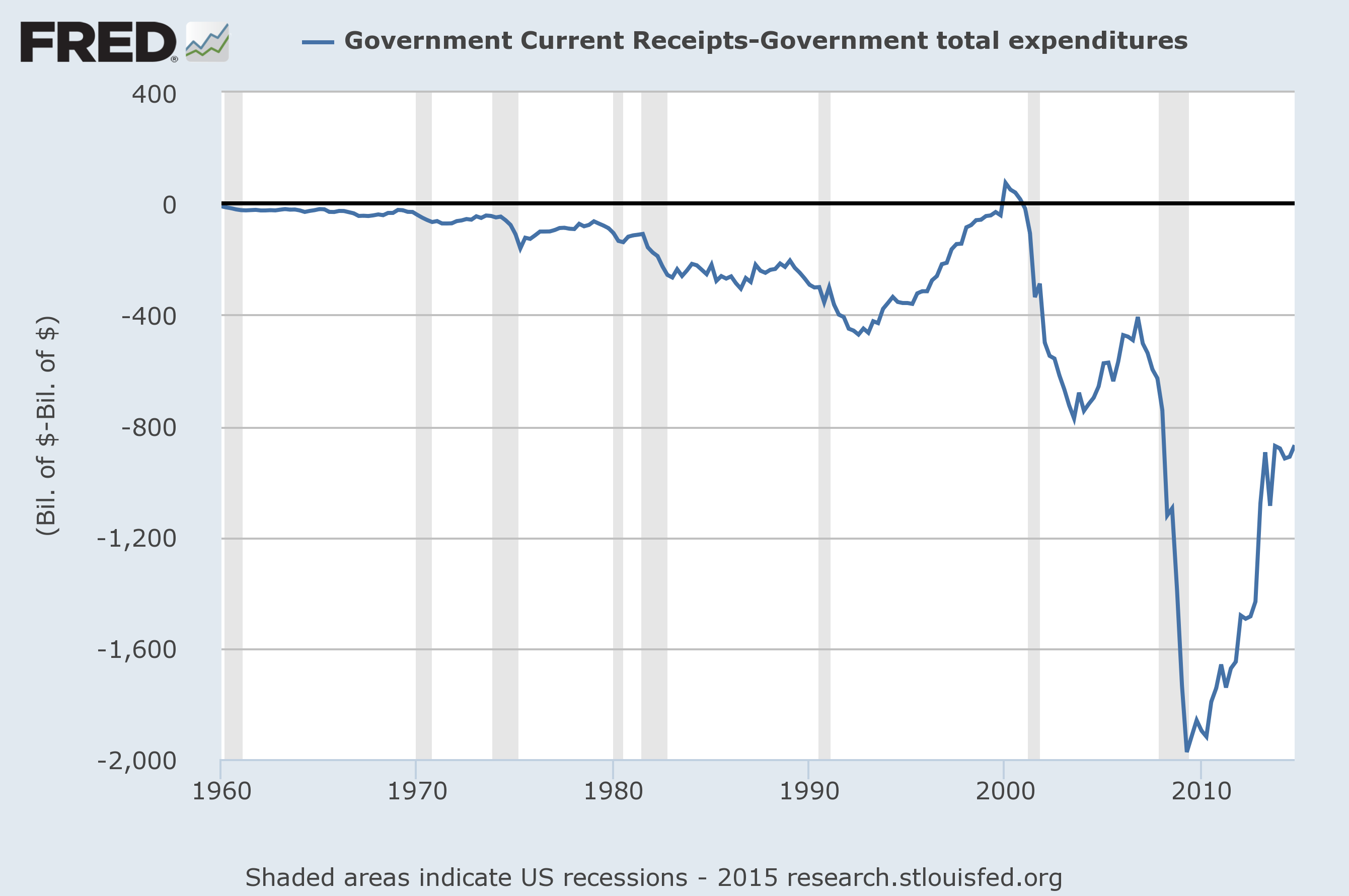

How about government saving? Again, we presently observe increasing saving (smaller deficits). Frankly, falling government deficits have been a drag on profit growth for a while, but that was offset by two things. One was a sharp deterioration in household savings, and the other was a failure of foreign savings to expand (i.e. the current account balance to deteriorate) despite a recovery in real investment.

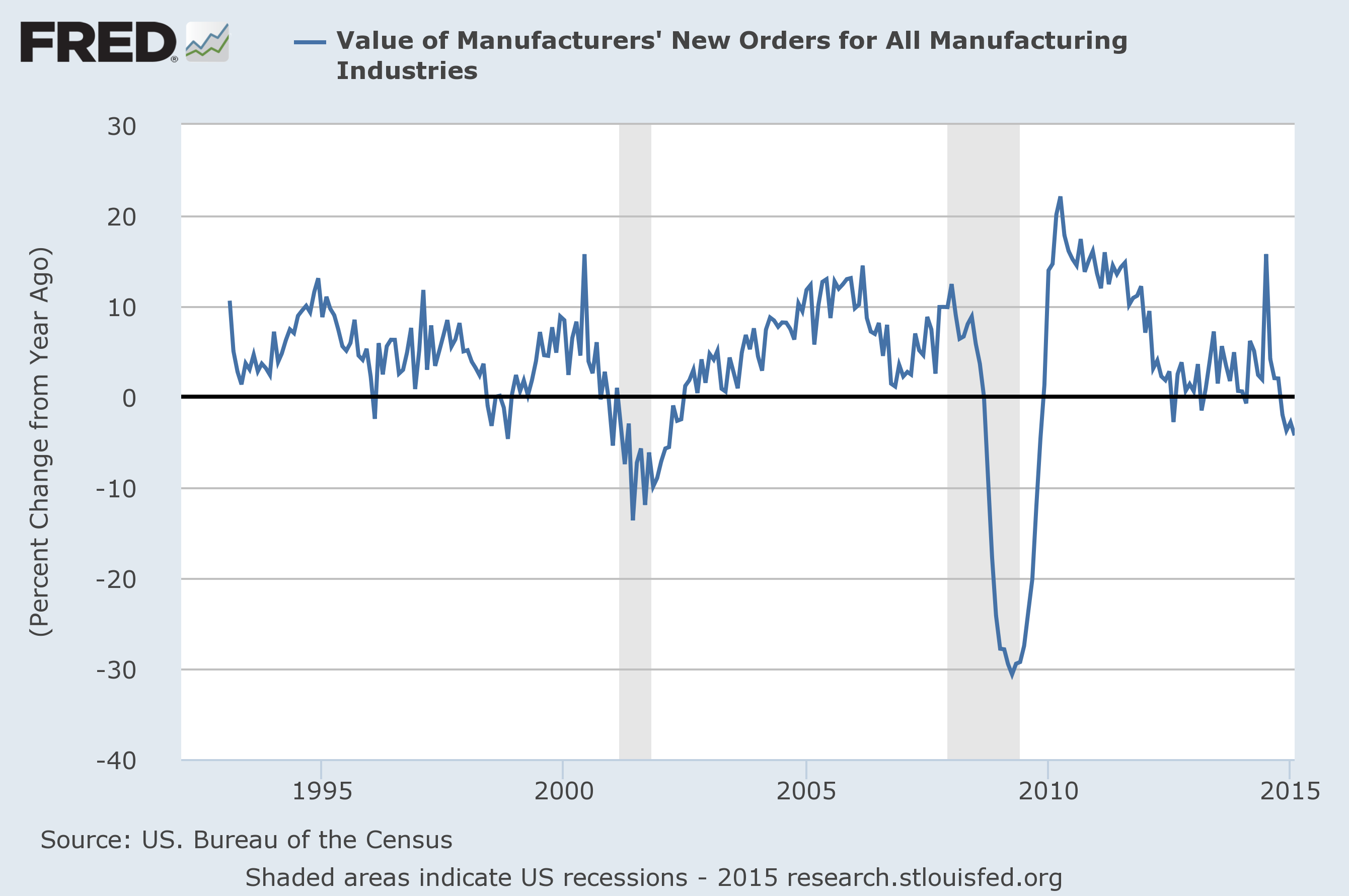

In short, corporate profits expand when gross domestic investment is growing strongly, the U.S. current account balance moves toward surplus (more exports, fewer imports), and the sum of household and government savings deteriorates. At present, all of these components are moving in the wrong direction from the standpoint of profit margins. Yet none of these components have moved so far that we would expect that direction to reverse. That’s another way of saying that the ladder that has supported the move to record high U.S. corporate profit margins is beginning to snap. It may be a long way down. I’ll emphasize again that our current market concerns are not dependent on this outlook for profit margins. Stocks are very long-term instruments, and essentially discount decades of future earnings, not just the next few years. The real difficulty with valuations is reflected in a variety of historically reliable measures that are well over double their historical norms. The central near-term concern is that elevated valuations are now joined with evidence of increasing risk-aversion among investors. Consider the profit margin argument to be a back-story and something to watch, not as the driver of our concerns. Even so, a great deal of investor confidence may be quietly resting on the assumption that current margins are permanent, so outcomes to the contrary could accelerate the re-valuation of stocks to less extreme levels. All of this will be interesting to watch. Meanwhile, we remain focused primarily on the joint condition of valuations and observable measures (market internals, credit spreads) that reflect the preference or aversion of investors toward risk. A few final charts will round out some of our economic concerns. As I’ve frequently noted, economic difficulties tend to emerge first in financial variables such as interest rates, credit spreads, and industrial commodity prices, followed by retail sales and survey measures of new orders and order backlogs, followed by production measures, followed by personal income, followed by new claims for unemployment, and generally confirmed much later by payroll employment. Being attentive to this sequence can be helpful in avoiding confusion if, for example, new orders, sales and production are falling but employment figures are generally upbeat for a while. The following chart captures some of our concerns on this front. Manufacturers new orders are now contracting at the fastest rate since the past two recessions. We don’t believe there's enough evidence to warn of a recession at present, but the data are clearly going in the wrong direction.

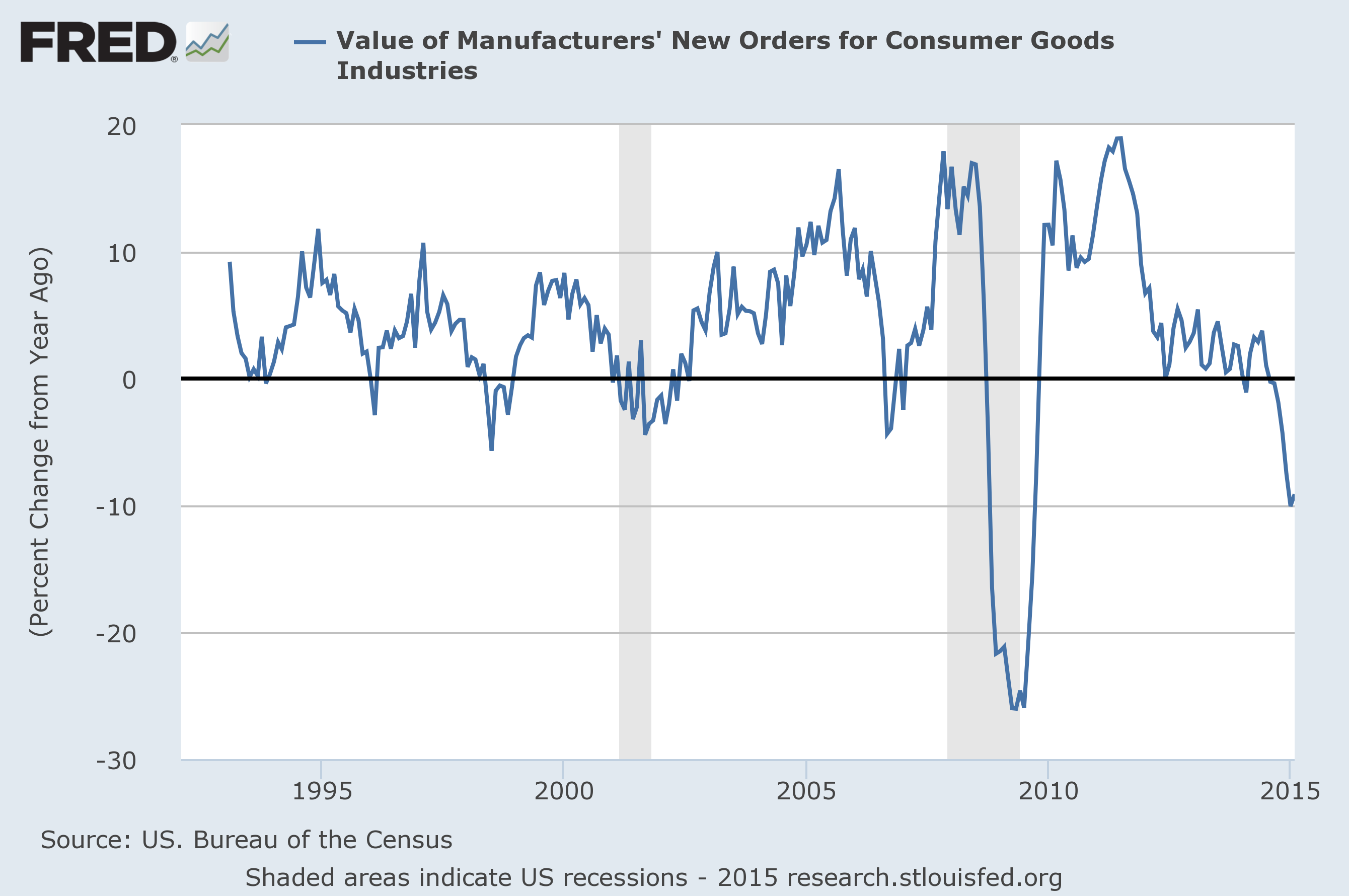

We also observe an abrupt contraction in new orders for consumer goods here, shown in the chart below.

I updated our own composite of economic conditions a few weeks ago. The chart below presents a similar index called the ADS Business Conditions Index (h/t the always resourceful Doug Short). While current levels have sometimes been observed outside of recession, our concern again is the abrupt deterioration, and the fact that the data are clearly moving the wrong way.

We’ll take our evidence as it comes, and in the event that investors shift back to a risk-seeking mode, the immediacy of our concerns will be deferred somewhat. Our goal is not to dissuade passive investors from their own discipline, provided that they carefully understand the typical size of market declines that complete the full market cycle (most bear market declines wipe out more than half of the preceding bull market advance, on average), and provided that they carefully align their investment portfolio with the horizon over which they expect to spend the funds. We do believe that investors with horizons of about 8 years or less are likely to experience net losses in equities over those horizons, coupled with a great deal of cyclical volatility, but our main points for passive investors are to temper your expectations about future returns, understand the potential cyclical risks, and align your portfolio duration with your spending horizon. Keep in mind that at a 2% dividend yield on the S&P 500, the effective duration of equities works out to about 50 years. At a more normal 4% dividend yield, the duration works out to be about 25 years. That means that an investor with a 25 year spending horizon could be comfortable being 100% in stocks at a 4% yield, but might best limit exposure to about 50% invested at a 2% index yield. That’s not market timing – that’s just duration matching. In our view, investors would be well served to consider their duration exposure sooner rather than later. My sense is that many investors are carrying far more equity risk and far longer duration than is appropriate for their investment situation, and it’s best to discover that before the market cycle is completed by a downturn. I can’t overstate that whatever a defensive investor might have “missed” in the late stages of the tech bubble, or the housing bubble, the 2000-2002 decline wiped out the entire total return of the S&P 500 – in excess of Treasury bills – all the way back to May 1996. The 2007-2009 decline wiped out the entire total return of the S&P 500 – in excess of Treasury bills – all the way back to June 1995. The intervening market gains didn’t mean a thing for investors who didn’t act at points of severe overvaluation to realize those gains. Doing so might have been frustrating over the near-term, but the completion of each cycle was ultimately very forgiving about exactly when an investor might have acted, particularly if the defensive action was at a point of market strength and overvaluation.The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |